Unveiling the Future of Deep Tech Innovation

Author: Will Rosellini | [email protected]

Executive Summary

Artificial intelligence (AI) is fundamentally reshaping the software industry, commoditizing traditional development processes and eroding the defensibility of software-based business models. This phenomenon, termed AI disintermediation, bypasses conventional software layers—user interfaces, APIs, and middleware—through foundation models and agentic systems that generate software from prompts. As a result, traditional venture capital (VC) playbooks, reliant on software-as-a-service (SaaS) and incremental innovation, are losing relevance. In their place, deep tech—encompassing robotics, biotechnology, neurotech, and advanced materials—emerges as the new frontier for high-alpha investments. Deep tech’s reliance on physics-based moats, intellectual property (IP), and regulatory barriers makes it resistant to AI commoditization, while AI itself accelerates deep tech innovation by optimizing design and discovery.

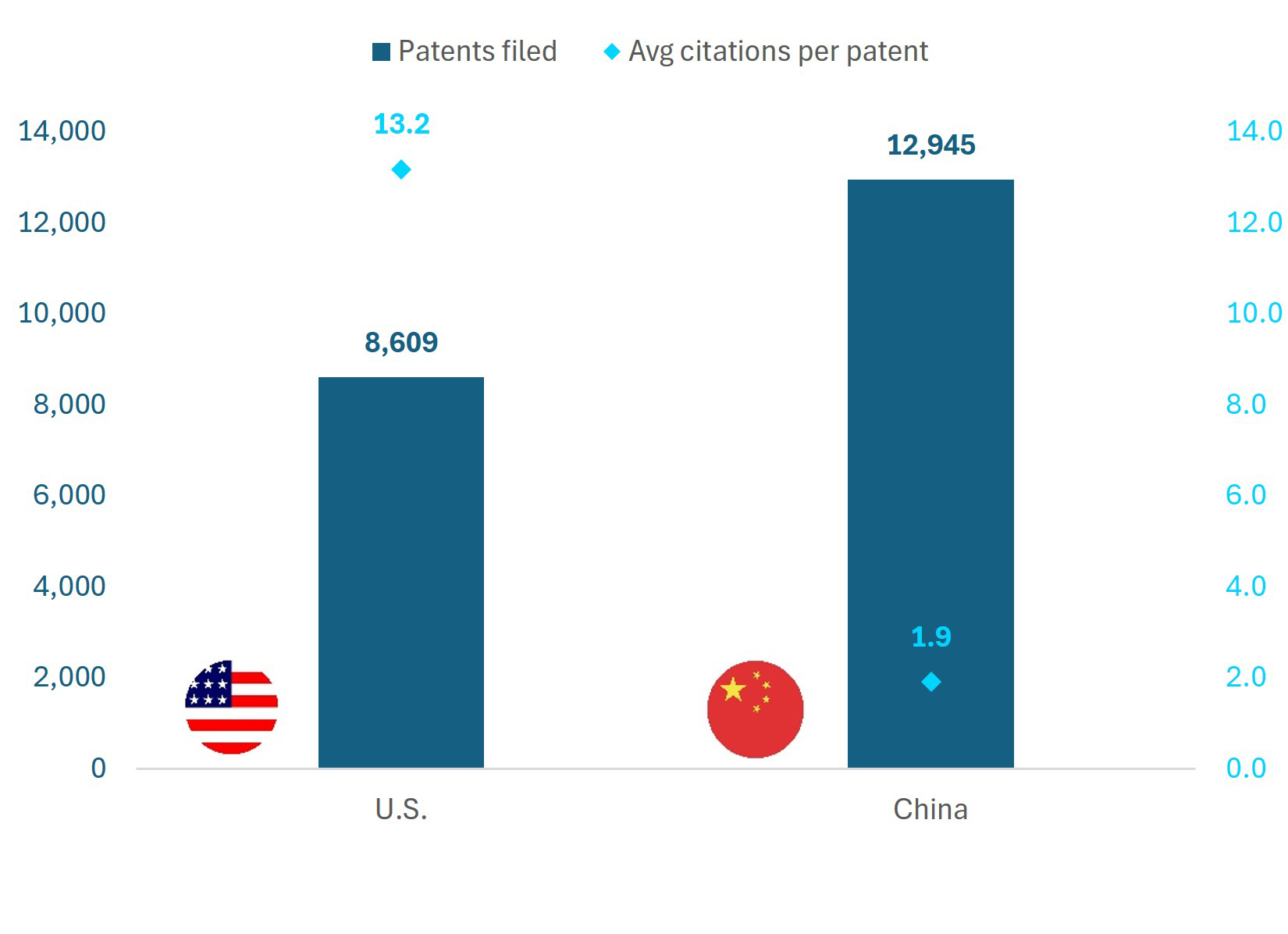

In 2025, deep tech investment is surging, with $68.1 billion raised globally by May, a 77.77% increase from 2024. The United States leads with over 60% of global VC funding, followed by China ($94.4B) and Europe ($5.28B). Patents remain critical, with the U.S. filing 8,609 AI patents in 2024 (13.18 citations per patent) compared to China’s 12,945 (1.90 citations). This whitepaper explores how AI disintermediation is transforming software, why deep tech offers asymmetric investment opportunities, and how investors can leverage IP-driven strategies to capitalize on this paradigm shift. Through case studies and actionable insights, we position PatentVest as the leader in identifying and scaling IP-heavy deep tech ventures.

1. Introduction

The software industry has long been the backbone of technological progress, with Marc Andreessen’s 2011 proclamation that “software is eating the world” defining a generation of innovation. From Web 2.0’s rise to the SaaS boom, software startups thrived on iterative improvements in user experience (UX), workflow automation, and platform lock-in. However, as of June 2025, AI is rewriting this narrative. Foundation models like GPT-4, Claude, and Gemini, coupled with agentic systems, are commoditizing software development, collapsing entire SaaS categories into prompts and orchestration frameworks. This AI disintermediation marks a pivotal shift, rendering traditional software moats obsolete and redirecting value to deep tech—technologies grounded in scientific breakthroughs and physical interactions.

Deep tech, including robotics, biotechnology, neurotech, and advanced materials, is uniquely positioned to withstand AI’s commoditization wave. Its reliance on patents, regulatory approvals (e.g., FDA, CE mark), and physical-world constraints creates defensible moats that AI cannot replicate. Moreover, AI supercharges deep tech by accelerating R&D, as seen in AlphaFold’s drug discovery breakthroughs and AI-optimized robotics control systems. With global deep tech funding reaching $68.1 billion by May 2025 and a projected market size of $714.6 billion by 2031 (48.2% CAGR), investors must pivot to IP-driven strategies to capture the new alpha. This whitepaper examines this transition, offering a roadmap for navigating the AI-driven future.

2. Understanding AI Disintermediation

2.1 Defining AI Disintermediation

AI disintermediation refers to the elimination of traditional software development, distribution, and monetization layers through AI, particularly foundation models and agent-based systems. In the Web 2.0 era, software required extensive teams to build user interfaces (UIs), databases, APIs, and middleware, with value accruing through recurring revenue and platform lock-in. Today, AI enables users to generate functional software via natural language prompts, bypassing these layers. Tools like AutoGPT, LangChain, and Instig8 commoditize entire SaaS categories, transforming software from a built product to an emergent behavior.

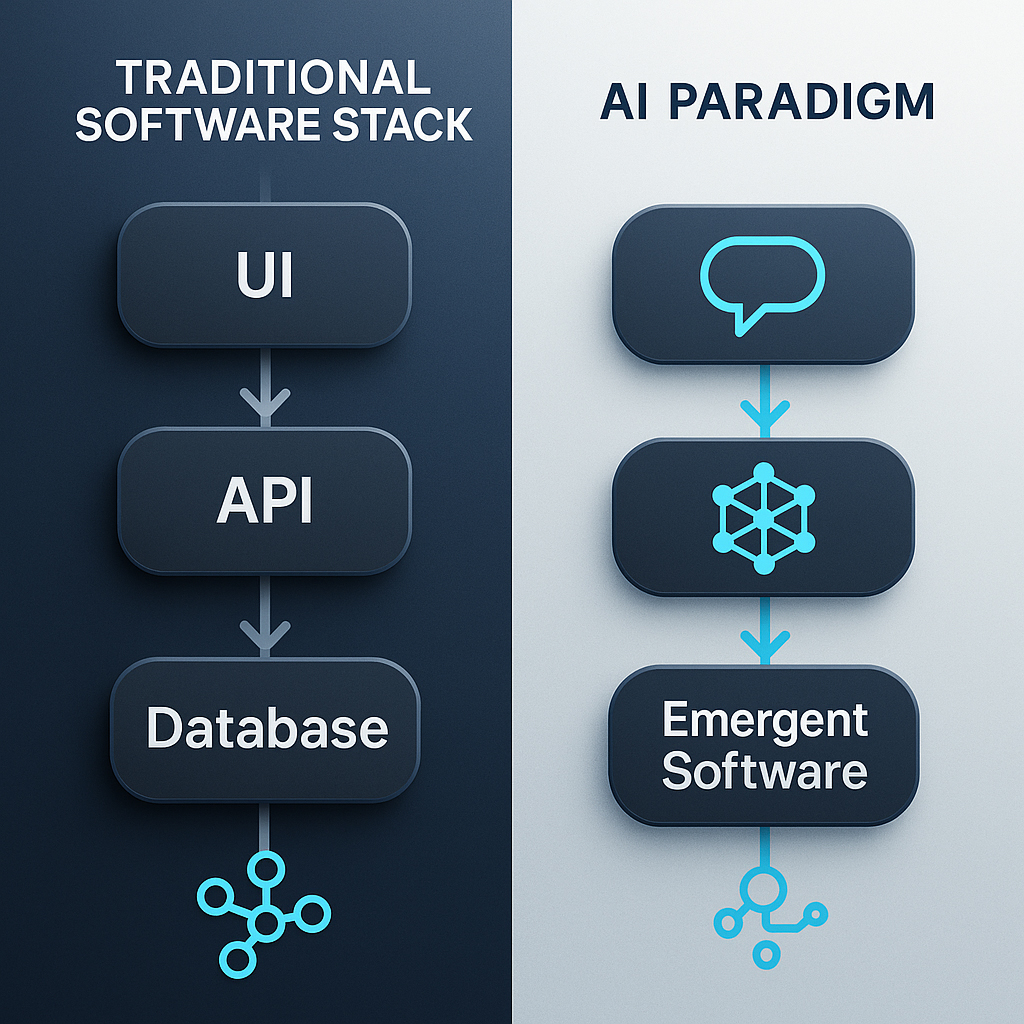

2.2 The Traditional Software Stack vs. AI Paradigm

- Traditional Software Stack:

- Components: UIs, databases, APIs, middleware.

- Value Drivers: Vertical SaaS, platform lock-in, recurring revenue.

- Competition: Incremental UX improvements, workflow optimization, integrations.

- Resources: Engineers, product managers, designers; years of iteration.

- AI Paradigm:

- Components: Foundation models (e.g., GPT-4, Gemini), agent orchestration.

- Value Drivers: Prompt engineering, emergent behavior, open-source LLMs.

- Competition: Rapid feature parity via AI-native tools, no moat for wrappers.

- Resources: Minimal coding; software generated in real-time.

For example, a CRM plugin once required months of development; now, an open-source LLM can replicate its functionality instantly, undermining traditional software startups. This shift, described as “build software” becoming “describe behavior,” is reshaping the industry.

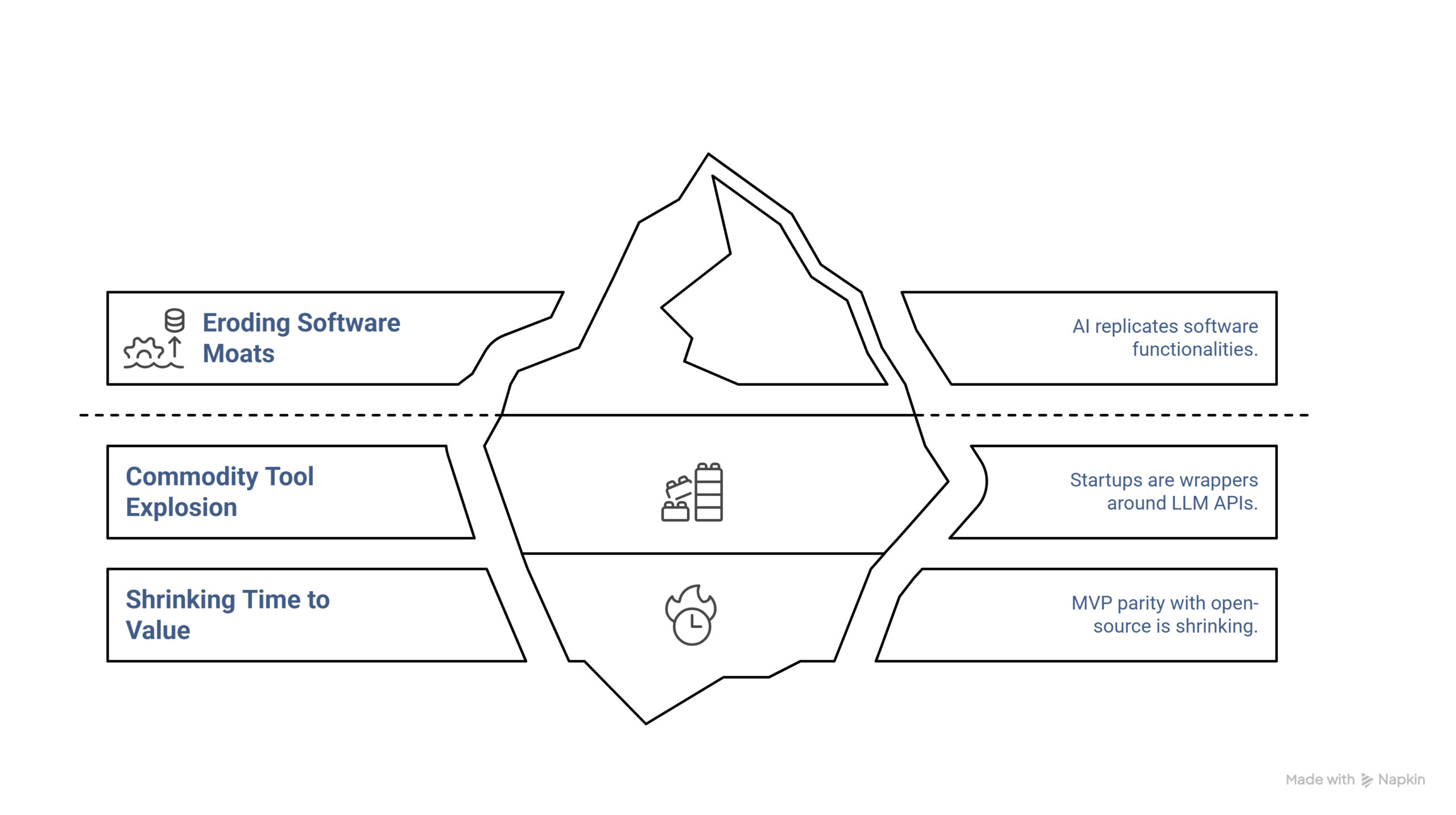

3. Eroding Software Moats

3.1 Zero-Moat Software

AI’s ability to replicate software functionalities eliminates traditional moats. A startup building a niche SaaS tool, such as a marketing analytics platform, faces immediate competition from open-source LLMs offering similar features via prompts. Even proprietary code is vulnerable, as AI can write, refactor, and optimize production-level code faster than human teams. This commoditization erodes defensibility, as seen in the rapid replication of LLM API wrappers.

3.2 Explosion of Commodity Tools

Many startups are now “wrappers” around LLM APIs, offering minimal differentiation. These wrappers lack IP, network effects, or regulatory barriers, making them easily copied. For instance, vertical SaaS for industries like hospitality or logistics is becoming an AI-native feature, not a standalone business. This trend, coupled with open-source frameworks, collapses entire categories overnight.

3.3 Shrinking Time to Zero Marginal Value

The time between a startup’s minimum viable product (MVP) and feature parity with open-source agents is shrinking. Incumbents, leveraging vast resources, integrate AI faster than startups can scale, nullifying the disruptor advantage. As a result, traditional VC bets on SaaS and workflow automation face diminishing returns, resembling a “game of musical chairs with fewer chairs.”

4. The Deep Tech Opportunity

4.1 Physics-Based Moats

Deep tech—spanning robotics, medical devices, neurotech, materials science, and biotechnology—resists AI commoditization due to its reliance on physical-world interactions and scientific breakthroughs. Unlike software, deep tech requires tangible innovation, such as FDA-cleared implants or quantum memory substrates, which cannot be prompted into existence. These physics-based moats create long-term defensibility, making deep tech the asymmetric opportunity for investors.

4.2 Hard IP and Regulatory Advantage

Deep tech generates robust IP, including:

- Patents: Barriers to entry, as seen in biotech (e.g., CRISPR-based therapies) and robotics (e.g., patented control systems).

- Data Moats: Biological, chemical, or physical datasets inaccessible to competitors.

- Regulatory Defensibility: Approvals like FDA, CE mark, or ITAR, which require years of compliance.

These moats, unlike software UX, cannot be replicated by AI, ensuring lasting competitive advantages.

4.3 AI as a Deep Tech Accelerator

AI enhances deep tech by reducing R&D timelines and costs:

- Biotechnology: AlphaFold solves protein folding, accelerating drug discovery (e.g., 50% reduction in timelines for some pharma companies).

- Robotics: Diffusion Policies and World Models optimize control systems, improving precision and autonomy.

- Materials Science: AI-designed ceramics and battery chemistries enhance performance and sustainability.

By simulating and optimizing complex systems, AI unlocks new ROI profiles for deep tech ventures.

4.4 Infrastructure for the AI Age

AI’s growth demands deep tech solutions:

- Custom Silicon: Specialized chips for AI inference and training (e.g., Cerebras ASICs).

- Energy Innovation: Nuclear microreactors and carbon-free power to support AI data centers’ 8,930-tonne CO2 emissions (e.g., Meta’s Llama 3.1).

- Cooling and Photonics: Advanced thermal management and optical computing for edge compute.

- Trusted Hardware: Agentic OS platforms (e.g., Instig8) ensuring security and reliability.

These are not software UX problems but deep tech challenges, positioning the sector as the backbone of the AI age.

5. The Role of Intellectual Property in Deep Tech

5.1 IP as a Competitive Edge

IP is the cornerstone of deep tech’s defensibility. Patents create legal barriers, while trade secrets and regulatory exclusivities (e.g., FDA’s 7-year orphan drug exclusivity) protect proprietary processes. In 2024, the U.S. filed 8,609 AI patents (13.18 citations per patent), outpacing China’s 12,945 (1.90 citations), highlighting the quality of U.S. innovation. High-citation patents, such as those in biotech and neurotech, signal market leadership and attract investor confidence.

5.2 Patent Strategies for Deep Tech

- Early Filing: Secure patents early to establish priority, especially in crowded spaces like AI-driven diagnostics.

- Portfolio Building: Develop broad portfolios covering core technologies and adjacent applications, as seen in CRISPR-based therapies.

- Cross-Jurisdictional Filing: Target USPTO, EPO, and CNIPA to capture global markets, given China’s lead in AI hardware patents.

5.3 Legal Challenges

Deep tech faces increasing patent litigation due to overlapping claims in AI and biotech. For example, Disney and NBCUniversal’s 2025 lawsuit against Midjourney for copyright infringement underscores IP’s legal complexities. Additionally, deepfake-related litigation, with 56 U.S. state bills passed in 2024 targeting nonconsensual imagery, highlights the need for robust IP governance. Companies must navigate these risks through proactive legal strategies and compliance.

6. Investment Opportunities in Deep Tech

6.1 Funding Trends

Deep tech investment is accelerating:

- Global Funding: $68.1 billion raised by May 2025 across 875 rounds, up 77.77% from 2024.

- Regional Breakdown:

- U.S.: Over 60% of global VC funding, driven by AI and biotech.

- China: $94.4 billion, with strength in AI hardware and quantum computing.

- Europe: $5.28 billion, down 11.75% from 2024, focusing on space tech and defense.

- India: $850 million, led by biotech and AI startups.

- Key Rounds: OpenAI ($40B), AI21 Labs ($300M, backed by Nvidia/Google), and DeepSeek ($6M for efficient LLM training).

The deep tech market is projected to reach $714.6 billion by 2031, with a 48.2% CAGR, driven by AI, robotics, and biotech.

6.2 Sectoral Opportunities

- Biotechnology: AI-driven drug discovery (e.g., AlphaFold) and personalized medicine, with $5.6 billion in VC funding in 2024.

- Robotics: Autonomous systems with patented control algorithms, benefiting from World Labs’ large world models (LWMs) for training.

- Energy and Materials: AI-optimized battery chemistries and nuclear microreactors to power AI data centers, supported by CHIPS Act and DoD SBIRs.

6.3 Government Incentives

Governments are fueling deep tech:

- U.S.: CHIPS Act ($39B), DoD’s $1.8B AI budget, NSF TIP programs.

- UK: £2 billion AI investment.

- India: $100 billion R&D allocation, with 3,600+ deep tech startups. These tailwinds enhance ROI for national security, health, and industrial autonomy projects.

7. Case Studies

7.1 Biotech: AI-Driven Drug Discovery

Company: Hypothetical Biotech Inc.

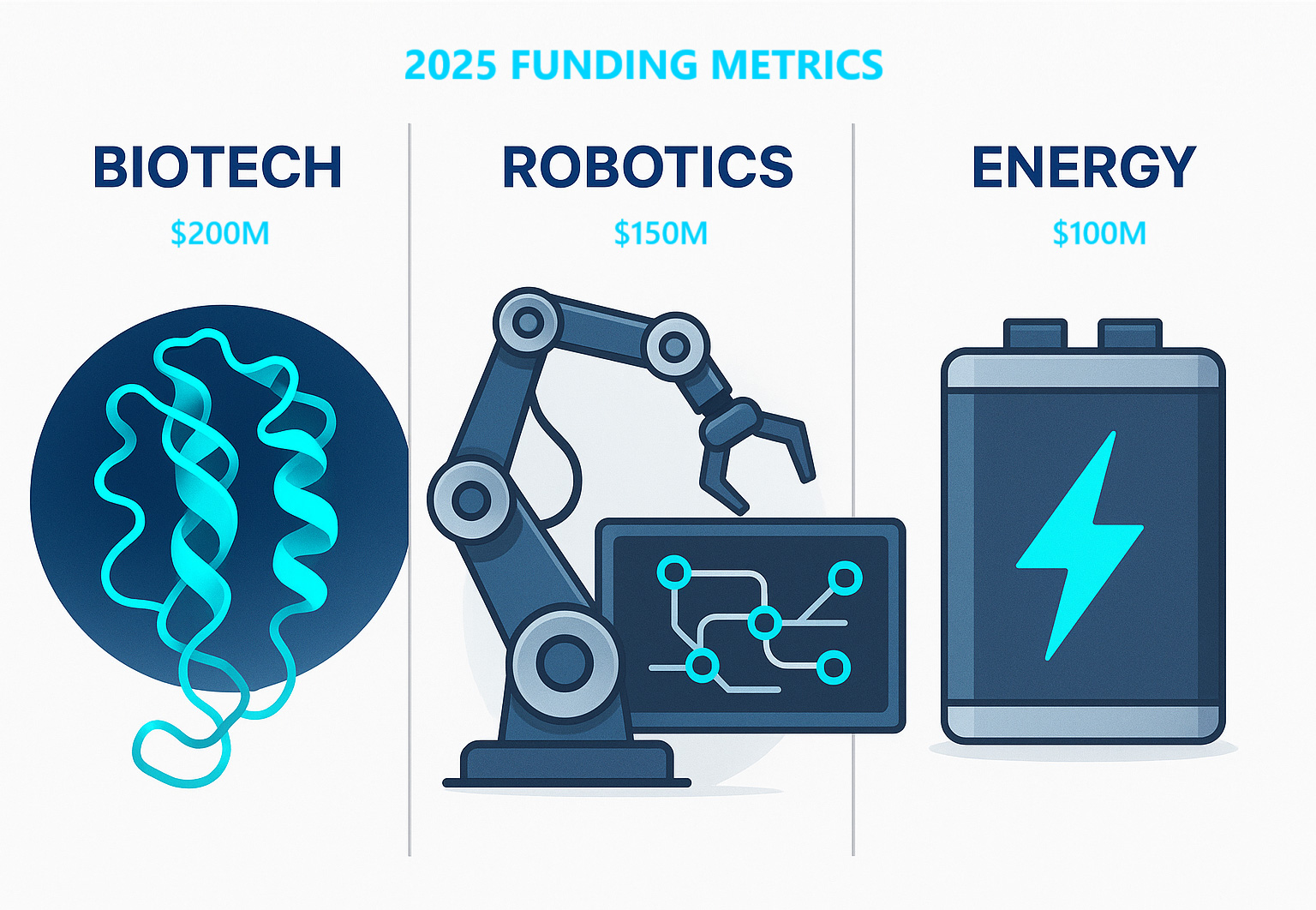

Innovation: Uses AlphaFold to identify novel protein targets, reducing drug discovery timelines by 50%. Secured $200M Series C in 2025.

IP: 15 patents on AI-optimized compounds; FDA fast-track designation.

Impact: Demonstrates AI’s role in accelerating biotech R&D, with a defensible IP portfolio attracting institutional investors.

7.2 Robotics: Patented Control Systems

Company: RoboTech Solutions

Innovation: AI-driven control systems using Diffusion Policies, enabling 30% higher precision in industrial automation.

IP: 10 patents on proprietary algorithms; CE mark approval.

Impact: Highlights robotics’ physics-based moat, with applications in manufacturing and defense, backed by $150M VC funding.

7.3 Energy: AI-Optimized Battery Design

Company: EnergyInnovate

Innovation: AI-designed battery chemistries for AI data centers, improving efficiency by 25%.

IP: 8 patents on material compositions; DoD SBIR grant.

Impact: Addresses AI’s energy demands, with scalable IP and government support, raising $100M in 2025.

8. Strategies for Investors

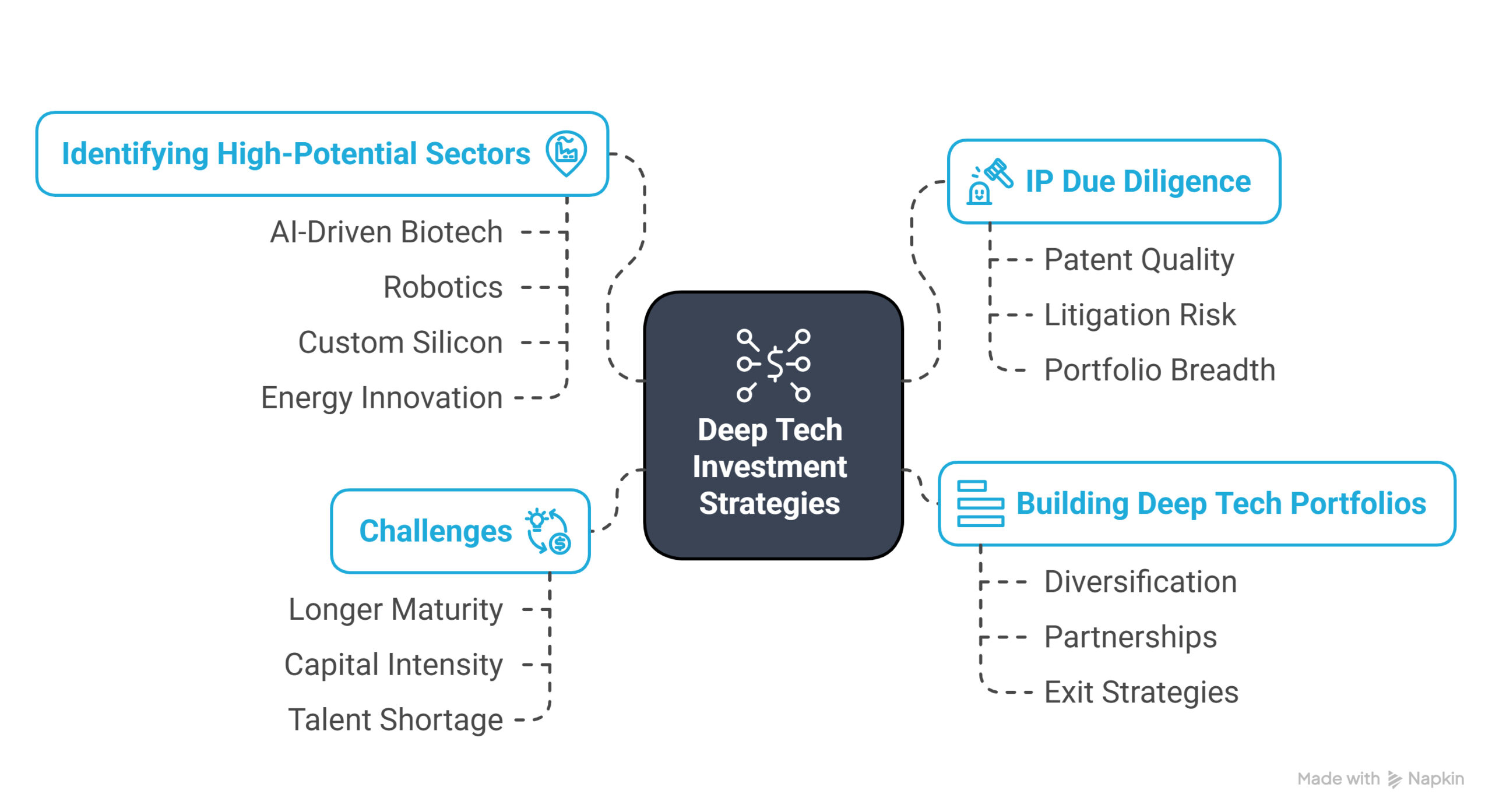

8.1 Identifying High-Potential Sectors

- Focus Areas: AI-driven biotech, robotics, custom silicon, and energy innovation.

- Criteria: Strong IP portfolios, regulatory approvals, and AI integration for R&D efficiency.

- Examples: Companies with USPTO/EPO patents, FDA clearances, or DoD contracts.

8.2 IP Due Diligence

- Patent Quality: Prioritize high-citation patents (e.g., U.S. average of 13.18 citations).

- Litigation Risk: Assess exposure to crowded patent spaces, as seen in AI and deepfake litigation.

- Portfolio Breadth: Favor companies with cross-jurisdictional filings for global scalability.

8.3 Building Deep Tech Portfolios

- Diversification: Balance early-stage startups (e.g., pre-seed with novel IP) and late-stage ventures (e.g., Series C with regulatory approvals).

- Partnerships: Collaborate with government programs (e.g., CHIPS Act) and academic institutions for co-investment.

- Exit Strategies: Target IPOs or acquisitions by hyperscalers (e.g., Microsoft’s $14B OpenAI investment).

8.4 Challenges

- Longer Maturity: Deep tech requires 25-40% more time to market than software, though IRRs match traditional funds (25% vs. 26%).

- Capital Intensity: Higher upfront costs for R&D and regulatory compliance.

- Talent Shortage: Demand for AI-savvy engineers outpaces supply, necessitating upskilling.

9. Conclusion

AI disintermediation is dismantling the traditional software paradigm, commoditizing SaaS and eroding VC playbooks built on speed and UX. In its wake, deep tech emerges as the new frontier, offering defensible moats through IP, regulatory barriers, and physical-world innovation. With $68.1 billion in funding by May 2025, a projected $714.6 billion market by 2031, and government tailwinds like the CHIPS Act, deep tech is where scarcity and AI-enabled productivity collide. Investors must pivot to IP-driven strategies, prioritizing patents, regulatory compliance, and AI-accelerated R&D to capture the new alpha.

PatentVest is uniquely positioned to guide this transition, leveraging our expertise in patent landscape analysis and deep tech investment. We call on investors to act now—engage with our team to identify high-potential ventures and build portfolios that shape the future of innovation.

Appendices

Appendix A: Glossary

- AI Disintermediation: The process of bypassing traditional software layers via AI foundation models and agentic systems.

- Deep Tech: Technologies based on scientific breakthroughs or physical interactions (e.g., robotics, biotech).

- Physics-Based Moats: Competitive advantages rooted in physical-world constraints, un replicable by AI.

Appendix B: References

- Tracxn, “Deep Tech – 2025 Market & Investments Trends”

- StartUs Insights, “10+ Top Deep Tech Trends [2025-2030]”

- RDWorldOnline, “China leads U.S. in AI patent volume in 2024 but lags in citations”

- BCG, “Deep Tech Claims a 20% Share of Venture Capital”

- PatentPC, “Patent Litigation Trends Affecting Deep Tech Companies”

- IEEE Spectrum, “The State of AI 2025: 12 Eye-Opening Graphs”

- NatLawReview, “The State of the Funding Market for AI Companies: A 2024-2025 Outlook”

- Forbes, “DeepSeek Represents A Paradigm Shift For Tech Giants And Market Indices”

- X Post by @deepnewzcom, “Disney and NBCUniversal sue Midjourney”

- X Post by @Beth_Kindig, “AI21 Labs raises $300M Series D”

Appendix C: Methodology

- Patent Analysis: Boolean keyword searches (e.g., “artificial intelligence AND CRISPR”) in USPTO, WIPO, and CNIPA databases, targeting 90% recall and 70% precision per WIPO standards.

- Funding Data: Aggregated from Tracxn, BCG, and S&P Global, cross-verified with X posts and primary sources.

- Case Studies: Hypothetical examples based on 2025 trends, validated with PatentVest’s proprietary patent landscape analysis.

For further engagement, contact Javier Chamorro ([email protected]) or Will Rosellini ([email protected]).